According to the Institute on Aging the ‘older adult’ population in the United States has increased from 11 percent (%) in 1985, to 13% in 2010 and is ‘expected to reach 20%’ by 2030. They reported that ‘65% of older adults with long-term care needs rely exclusively on family and friends to provide assistance.’ And that ’50% of the elderly who have a long-term care need but no family available to care for them are in nursing homes, while only 7% who have a family caregiver are in institutional settings.’

https://www.ioaging.org/aging-in-america

According to the U.S. Census Bureau, in July 2015, 47.8 million Americans were age 65 and older, accounting for 15% of the total population. Their median household income was $38,515; and their median net worth was $170,500. Those in poverty were 8.8% down from 10% in 2014. In 2016, about 58% of the population age 65 and older was married.

https://www.census.gov/content/dam/Census/newsroom/facts-for-features/2017/cb17-ff08.pdf

The U.S. Census Bureau American Housing Survey (AHS) reported about 3 in 4 people in the United States live in houses (detached, attached or mobile homes) and about 1 in 5 live in apartments. The National Center for Assisted Living says the average move-in age is 84. People are living longer and spending a substantial part of their years in retirement.

Definitions

Home or Apartment (traditional): A residential place owned or rented which can be located in a city or in a country or rural area. They typically have several more rooms (bedrooms, dining, bathrooms, halls, living, office, etc.) than senior living options. Most have a yard or outside area that requires upkeep by the occupant; and is often more than 15 minutes from emergency help.

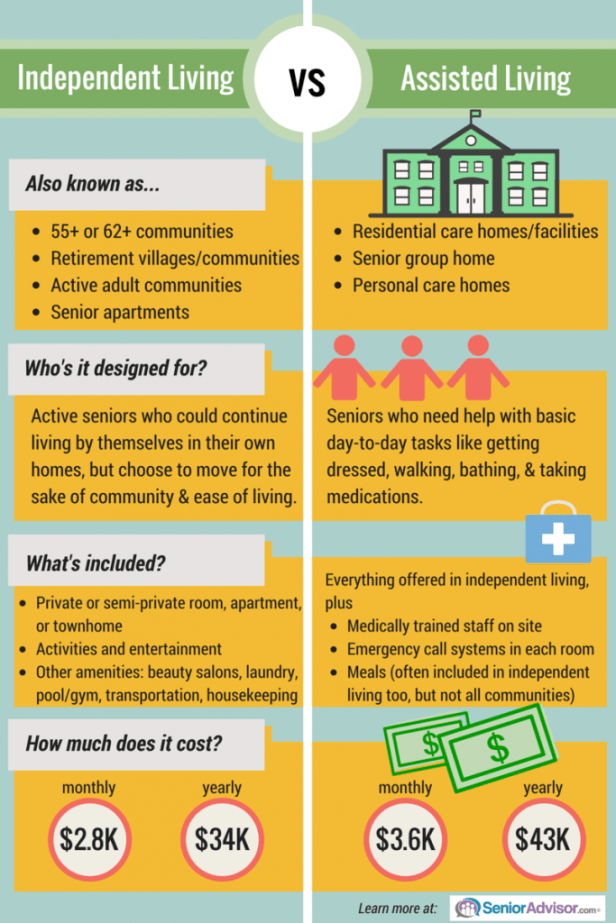

Senior Living Community Apartment or Townhome (independent living): relatively independent living with certain assistance to residents. Typically a quality senior community provides most of the following: 24-hour staffing, meals, housekeeping and laundry, entertainment and exercise programs, wellness classes, onsite home health services, medication assistance or reminders, courtesy transportation and or assistance with certain long-term care needs as bathing, dressing and haircare.

Assisted Living: Provides more personal care services than a home or independent living communities, but less than around-the-clock medical care such as in a nursing home. They should include 24-hour staffing, 3 meals served daily, personal care, medication administration and management, special nutrition help, transportation programs, housekeeping and laundry, long-term care needs assistance (bathing, dressing, grooming), incontinence care and security.

Considerations for Living Options for Elderly Parents

The decision to enter or place a loved one in the different setting of an assisted living facility is a difficult but frequently unavoidable one. The following sections could provide help in that decision process as to which setting may be best between a traditional home or assisted living.

I Current Living Status

- Are you single or married or have a roommate?

- Are you on Medicare or Medicaid?

- Do you live in a traditional home or apartment, a fully planned unit development (PUD), senior living community or in an assisted living residence?

- Are you working part-time, and if so, should you be involved in these activities?

- If you work in a family owned business, will it continue after you cease to be a part of it?

- Are you (or your spouse) able to drive or transport yourself to routine stores and doctors’ offices without any assistance?

- Are you (or your spouse) able to totally care for yourself without any assistance?

- Does your current living place allow reasonably quick access to emergency care?

- Are you at a significant higher risk of death or long-term disability in your current residence rather than at an assisted living facility or nursing home?

If you or your parent requires care for daily living tasks, or are concerned about answers to one or more of the above continue to the following sections. According to Kaplan’s Long-Term Care and Partnership Program Course (2018), ‘about 70% of individuals over 65 will require some kind of long-term care services in their lifetime… The Department of Commerce reports that 8.8 million Americans over age 65 receive long-term care of some type… 1.3 million are in nursing homes.’ U.S. life expectancy is about 78 years (longer for a non-smoker).

The Kaplanlearn.com Long-term Care course reports from the U. S. Department of Health and Human Services that of patients that stay in Nursing Homes, 31% are in less than a month, 21% 1 to 3 months, 11% 3-6 months, 7% 6-9 months, 5% 9-12 months, 10% 12-24 months and 11% over 3 years. Thus, the odds are about 8 in 10 will not be in a nursing home for more than a year until their death.

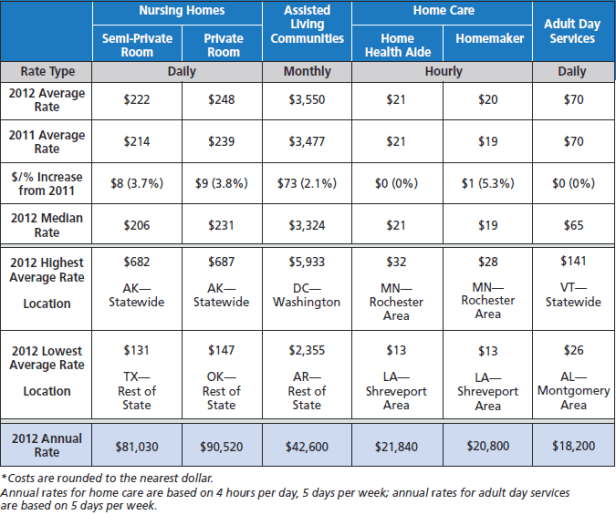

Assisted living typically fills a gap between traditional home life or home care assistance and nursing homes. The National Care Planning Council (NCPC) states that “Instead of the hospital environment of a nursing home, newer assisted living facilities look more like apartment buildings with private rooms or suites and locked doors. Instead of a nurse’s desk, there is a help desk. And instead of a hospital-like lounge area and sterile cafeteria, assisted living has gathering areas with couches, fireplaces, gardens, atriums, etc. Central dining areas look more like banquet rooms… Frequent outings are also planned.” The NCPC reports that the average stay in Assisted Living (residential adult care, community based retirement facilities, adult homes, etc.) was 2.5 to 3 years according to a 1999 survey. Currently (2018) the stay is about 3 years at a cost of about 65% of a nursing home or about $ 3,600 per month (2018) and according to Caring.com expected to rise to more than $ 4,800 a month by 2026.

https://www.longtermcarelink.net/eldercare/assisted_living.htm

II Current Health Status

a. What kind of help do you or your loved one(s) need? Do you, your spouse or parent(s) require help with one or more of the following? Bathing, Dressing, Toileting or Continence (ability to control bowels and bladder), Eating, Transferring (to bed or chair), Medicating and or traveling for routine groceries and grooming.

b. To qualify for Long Term Care Insurance (from an Insurance Company), the policy owner or one having power of attorney must show that the insured needs substantial assistance with at least two of six daily living activities (eating, bathing, dressing, toileting, continence and transferring) and the condition must be believed to last at least 90 days.

c. Often a loved one requiring care can use At Home Care to meets their needs. However, more often individuals choose Assisted Living arrangements rather than At Home Care because their needs cannot be meet at home, on a part-time basis, they don’t feel at-home care will be the safest choice, they want to enter while the setting will be familiar and their choice, or some other reason.

d. What is your current life expectancy (is it adjusted for your current health)?

The average 80 year old is expected to live 8.5 more years. Link to Life Expectancy Calculator at Social Security website:

https://www.ssa.gov/planners/lifeexpectancy.html

e. The typical Long Term Care policy requires the insured to be less than age 80 and in fairly good health. Though you may not want, need or qualify for this coverage, it is important to see what would make an individual unqualified to purchase coverage due to their health because this also provides a view at serious conditions which lead toward the need for care.

f. The usual Long-Term Care policy will state roughly as follows (this is from a top insurer’s application): “This is not Medicare Supplement Coverage… LTC policies are designed to provide coverage for one or more necessary or medically necessary diagnostic, preventive, therapeutic, rehabilitative, maintenance, or personal care services, provided in a setting other than an acute care unit of a hospital, such as in a Nursing Facility, in the community or in the home. The Policy provides coverage in the form of an expense reimbursed benefit for covered qualified long-term care expenses, subject to benefit eligibility, policy limitations, elimination periods and daily and lifetime policy maximums… Elimination Periods are usually 20, 30, 90, 180 or 365 days.” Policy Lifetime Maximum benefit periods are often 2 to 5 years; though some offer up to 7 or 10 years or even unlimited daily reimbursements.

g. Long Term Care Policy/Application continued: There is usually a difference in coverage for at Home or Community-Based Care (Non-Institutional) and or an Assisted Living Facility versus in a Nursing Facility (Institutional). Eligibility questions for coverage asked if the insured needs ‘assistance or supervision to perform any of the following activities: bathing, dressing, eating, toileting, bowel, bladder control, moving; and Do you use any walker, wheelchair, oxygen… Have you ever been diagnosed or treated for… alzheimer’s, chronic memory loss… Within the past two years, have you had a stroke or used insulin to control diabetes… Within the past five years have you consulted with a health care professional (physician, doctor, etc.) or been treated for heart attack, heart surgery, chest pain, stroke, cancer, tumor, diabetes, anxiety, depression, asthma, arthritis, joint fracture, pain in the muscles of joints… or for any reason not stated?” (Answering yes to any certain one of these could change a rating or cause the proposed insured to be declined or denied for coverage).

h. Eligibility for Payment of Benefits: Eligible for benefits when you “are unable to perform without Substantial Assistance from another individual 2 or more of the Activities of Daily Living due to a loss in functional capacity which is expected to last at least 90 days; or have suffered a Severe Cognitive Impairment.”

Eligibility is confirmed at the Insurer’s expense usually by medical records.

The Activities of Daily Living include Bathing, Continence, Dressing, Eating, Toileting, and Transferring and are defined as follows:

- Bathing, means washing Yourself by sponge bath or in either a tub or shower, including the task of getting into or out of the tub or shower.

- Continence, means Your ability to maintain control of bowel and bladder functions; or when unable to maintain control of bowel or bladder functions, the ability to perform associated personal hygiene (including caring for catheter or colostomy bag.)

- Dressing, means putting on and taking off all items of clothing and any necessary braces, fasteners, or artificial limbs.

- Eating, means feeding Yourself by getting food into Your body from a receptacle (such as a plate, cup or table) or by a feeding tube or intravenously.

- Toileting, means getting to and from the toilet, getting on and off the toilet, and performing associated personal hygiene.

- Transferring, means moving into or out of a bed, chair or wheelchair.

Severe Cognitive Impairment means Cognitive Impairment such that You require Substantial Supervision to protect Yourself or others from threats to health and safety. Cognitive Impairment means a deficiency in a person’s:

- Short or long-term memory;

- Orientation as to person, place, and time;

- Deductive or abstract reasoning; or

- Judgment as it relates to safety awareness.

The loss or deterioration of intellectual ability is determined using reliable tests and clinical evidence demonstrating the impairment. Loss of intellectual ability can result from Alzheimer’s Disease or similar forms of senility or irreversible dementia or other mental illness.”

i. Other factors that affect or have affected your current health include excess unhealthy choices and deficiencies in important nutrients.

III Medicaid or Medicare

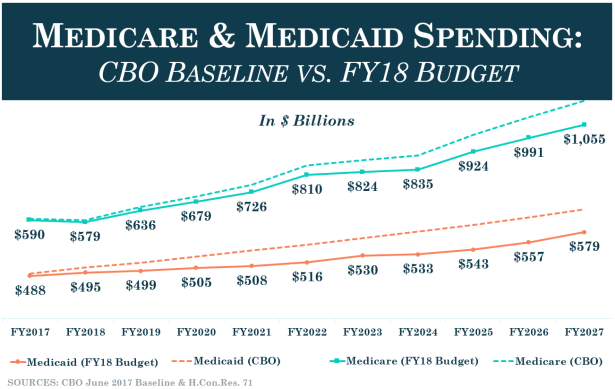

The population of the United States is about 329 million people (Dec. 2018). According to U. S. Centers for Medicare & Medicaid Services (CMS), in August 2018 over 73 million Americans were enrolled in Medicaid and CHIP (Children’s Health Insurance Program). Children make up over 35 million of this total; thus, about 38 million adults are on Medicaid. About 17% of those on Medicaid also are enrolled in Medicare. Approximately 56 million are on Medicare, almost 48 million by age (age 65 or older) and 9 million due to a disability.

- Medicaid (State Control with Federal Guidelines): According to the government’s Medicaid.gov site, “Medicaid provides health coverage to millions of Americans, including eligible low-income adults, children, pregnant women, elderly adults and people with disabilities. Medicaid is administered by states, according to federal requirements. The program is funded jointly by states and the federal government.”

https://www.medicaid.gov/index.html

Medicaid pays for long-term care ONLY for the POOR or who have become poor after paying for medical expenses, nursing homes and transferring assets in accordance to the law.

Adults EXEMPT from Out-of-Pocket Cost are: Individuals living in an institution who have only a minimal amount of assets/funds required for personal needs ($2,000 or less); or individuals receiving hospice care.

Keep in mind hospice care DOES NOT PAY for assisted living or nursing home Room and Board. Hospice covers physician services, aides and support related to the terminal illness.

Medicaid CMS Headquarter: 1-877-267-2323

Link to State Contacts below:

https://www.medicaid.gov/about-us/contact-us/contact-state-page.html

ASSET LIMITS to qualify for MEDICAID: (Vary some by state)

Income: all is counted including Social Security, veteran’s benefits, wages, pensions, interest and dividends, IRA distributions. Most states require a MAGI below $ 2,250 single or 3,300 married.

Cash: About $ 2,000 (13% of Americans live in 100% poverty)

Home: $ 500,000 exclusion toward your home in many states if occupied by applicant or spouse.

(Home value varies by state; over $800,000 in several states. Except for certain circumstances, such as a child living in the home from at least 2 years prior to transfer or a disabled child; there is a penalty for transferring a home within a 5 year period – Deficit Reduction Act of 2005.)

Car: One automobile in many states; Funeral: $ 1,500 pre-planned funeral plan and burial plot.

Personal Property: which is essential for self-support.

Life Insurance: Term policies are excluded, but cash value polices are included.

https://www.medicaidplanningassistance.org/find-a-medicaid-planner

2. Medicare: Federal Control

1-800-Medicare (633-4227)

The average benefit per enrollee in 2017 was approximately $ 13,000 (Part A: $ 5,000; Part B $5,650; Part D $ 2,350).

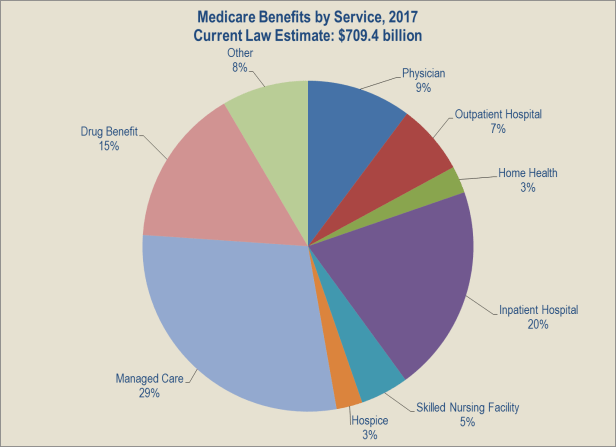

Part A benefits include in Hospital with various co-insurances after 60 days; skilled Nursing Facility, but NO BENEFITS after 101 days; certain limited Home Health Services; and Hospice care.

Part B benefits include physician and outpatient care, medical supplies, home health and preventive services. The benefits are paid basis on reasonable averages and excess cost must be paid for by the individual (or a Medicare Gap or Advantage plan which is design to cover the excess charge).

Part C (or Medicare Advantage) is a private insurance policy, such as a Managed Care HMO that replaces Part A and Part B for health and prescription drug coverage. It will vary by premium and insurer. There are also less popular Fee-for-service Part C plans.

Part D benefits include outpatient prescription drugs.

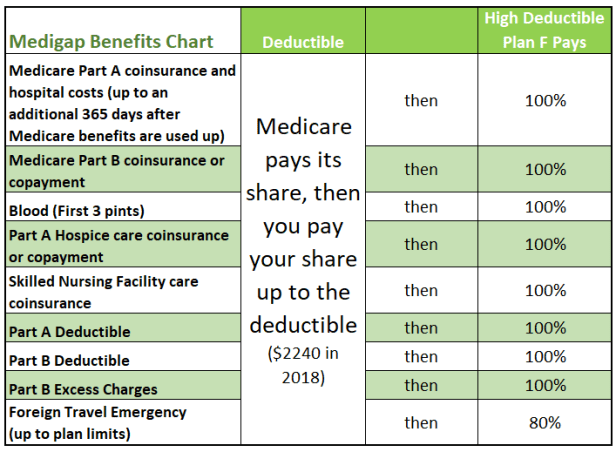

Medicare Medigap Plans: there are up to 10 standard plans offered in each state. There is no difference in coverage under the same Letter plan offered by any Insurer – the difference is only in the premium, services and financial strengths. Starting June 1 2010, plans E, H, I, or J were no longer available to buy. Most Medigap plans do not offer creditable drug coverage. Every Medigap policy must follow federal and state laws. Only plans F and G cover 100% of ‘Excess Charges’ related to Part B (doctor’s fees, etc.). Plan F offers a high-deductible option to lower premium costs ($ 2,300 in 2019). Some of the plans don’t cover foreign travel.

According to Medicare.gov, Starting January 1, 2020, Medigap plans sold to new people with Medicare won’t be allowed to cover the Part B deductible. Because of this, Plans C and F will no longer be available to people new to Medicare starting on January 1, 2020. If you already have either of these 2 plans (or the high deductible version of Plan F) or are covered by one of these plans before January 1, 2020, you’ll be able to keep your plan. If you were eligible for Medicare before January 1, 2020, but not yet enrolled, you may be able to buy one of these plans

IV Costs of Living Options

There are primarily SEVEN Senior LIVING OPTIONS for the elderly:

- Living in your current residence with or without at-home care.

- Purchasing or leasing a home or apartment with the option of at-home care.

- Living with a child or loved one with the option of at-home care.

- Board and Care Homes owned and operated by groups, agencies or a private company. They consist of several senior adults living in a single-family home. They are usually not covered by Medicare or Medicaid.

- Continuing Care Retirement Communities (CCRC) or Life Plan Communities (LPC) which provide ALL levels of housing and treatment from Independent Living (cottages or apartments) to Assisted Living (apartments connected to a main hallway and facility) to Memory Care (Memory Loss) to Skilled Nursing (Nursing Home).

- Assisted Living facilities provide options from shared rooms to private one and two bedroom apartments. They are set up to provide assistance with daily tasks such as bathing, dressing, medicating and eating. They provide all meals, social activities and light housekeeping. Typically there are about 5 or 6 residents per staff person.

- Nursing Homes provide around-the-clock medical care and are mainly for long-term stays until death. They are less private than assisted living and are the most expensive option. They often have a hospital feel to them.

This section will examine the pros, cons and costs for at-home care and assisted living.

- At-Home Care:

At-Home Home Health Care includes Medical and Non-Medical Care such as Rehabilitation, Injections and Medication management, Catheter or ventilator care, Diet/health management, and other services to meet daily needs. At-Home In-Home Care includes Cooking, Cleaning, Laundering, Dressing, Grooming, Grocery shopping, Transferring, and Medication assistance.

- Personal care: Bathing, eating, dressing, toileting, grooming

- Household care: Cooking, cleaning, laundry, shopping

- Health care: Medication management, physician’s appointments, physical therapy

- Emotional care: Companionship typically from aids, friends, family members

Indeed.com lists the average pay for a Caregiver as $12.28 per hour or about $23,400 per year. Jobtomic.com advertises ‘$15-27/Hr Caregiver Jobs – No Experience Required.’ A 2016 Genworth Financial study the actual cost to the payer for a caregiver to come to your (or your parent’s) residence is between $16 and $28 per hour if you go through an agency with a national median rate of $125 per day. Some independent caregivers will negotiate hours and pay.

Average Annual Costs for At-home Caregivers:

At 3 days a week at 4 hours a day = $ 11,500

At 5 days a week at 4 hour days = $ 19,000

At 7 days a week and 8 hour days = $ 54,000

24 hour continued care = over $ 140,000 for non-living in caregivers

24 hour continued care = over $ 40,000 for living-in caregivers

Average MONTHLY COST: $ 750 (Utilities, maintenance, groceries, grooming) + $ 1,550 (20 hours a week of paid help) = $ 2,300 per Month + {mortgage, property taxes, insurance} or Rent.

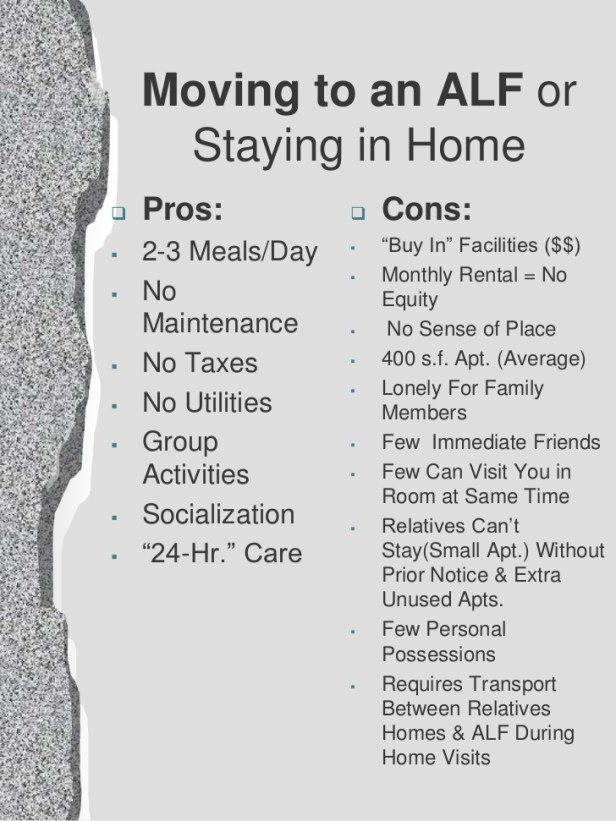

PROS:

The familiar environment of your home

Cannot be forced out of your residence due to personally, physical or cognitive skills

Often less experience than found in Assisted Living or Nursing Home

Typically no contract is required so you can change hours to fit your budget

Home Care Agencies can screen/hire/fire (but more expensive than private hire)

Flexibility in your schedule (when to eat, shower, dress, etc.)

Flexibility for the family to help

CONS:

Personal Care Assistants (PCA) are not licensed and have varied levels of training

Turnover rate is higher than for Assisted Living/Nursing Facilities

Less structured environment than in Assisted Living/Nursing Facilities

Often there is no care during the night

Some feel like a stranger is in their house

Often a lot of responsibility for a caregiver and family

Many caregivers may not be able to lift patient after a fall or handle an emergency

Adult children or grandchildren may not provide required or estimated care

Possible isolation from others

Assisted Living Facilities (below)

2. Assisted Living

Assisted Living Facilities (ALF) or residences provide a group living environment with options for privacy, while receiving care with activates of daily living (ADL) or needs. AssistedLivingFacilities.org has a directory of over 36,400 assisted living communities in the United States. Medicare rarely covers any assisted living cost.

- Personal care: Bathing, eating, dressing, toileting, grooming

- Household care: Cooking, cleaning, laundry, shopping

- Health care: Medication management, physician’s appointments, physical therapy

- Emotional care: Companionship, social events, conversation, transportation, security

Assisted living is for elders who need help or will soon need help with daily living tasks, but do not need continual 24 hr. care. ALF provide all maintenance and lawn upkeep, utilities, programs, medication management, laundry, housecleaning, meals and certain transportation. They offer caregivers on site 24 hours a day.

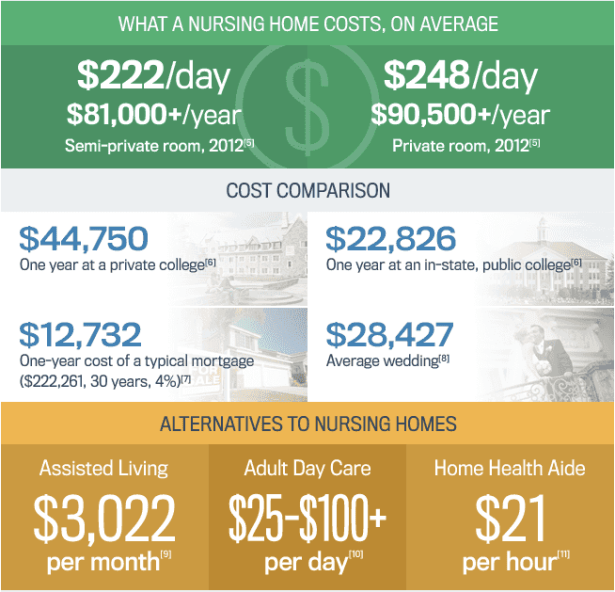

Average Annual Costs for Assisted Living Facilities:

Varies according to state and facility, example California average according to 2016 Genworth report was $4,000 per month. Caring.com reported that the U. S. average was $ 3,750 a month in 2017, up from the $ 3,500 2014 average.

Average MONTHLY COST: $ 3,800 or $ 45,600 per year for one bedroom.

Average MONTHLY COST: $ 4,700 or $ 56,400 per year for two bedrooms.

COSTS = Rent (room type fee) + Care (respite, low, high needs) + other fees (community, etc.)

PROS:

24 hour on site monitoring and staff (On-site licensed medical personnel)

Typically better trained workers with less turnover than at-home caregivers

Able to call more staff members to Pick up or Transfer a senior adult

More reliable schedules and practically guaranteed daily care with bathing, dressing, eating

They take care of ALL MAINTAINCE and at least 2 Meals every day

Home-like setting with opportunity to socialize and attend planned activities

Much lower cost than Nursing Home

Often lower cost than maintaining home and paying for at-home care

Transportation (included in cost) to shopping, religious services, etc.

Greater Safety and personal monitoring

Often better Nutrition (adjusted from some members) and Fitness programs

CONS:

More structured environment than at home

Some have trouble adjusting to new group setting and policies

Higher cost than having part-time caregivers at home

Two bedroom suites are expensive

Children or grandchildren may not be able to visit as easy or in large numbers

Cannot have large personal events on site, such as family Christmas or Thanksgiving

Must sign a contract and subject to removal due to non-payment, or physical or cognitive skills

Most must move to Memory Loss Facility or Nursing Home or to a private home at some point

V Some Questions and Various Links

Does your current residence provide ease of use and maintenance?

How are medical emergencies handled?

What happens if you have a heart attack, stroke or fall?

Can reasonably immediate assistance be provided before emergency services arrive?

Is there a nurse on the facility?

Are two or three meals prepared for you at this location?

What kind of care is available at night?

How does each of you feel about these options?

https://www.conciergecareadvisors.com/senior-living-options/

https://www.aarp.org/caregiving/home-care/info-2018/hiring-caregiver.html

https://www.caring.com/articles/cost-of-assisted-living

https://www.morningstar.com/articles/823957/75-mustknow-statistics-about-longterm-care.html

National Care Planning Council link below

“We are the most comprehensive resource for Eldercare, Senior Services and Care Planning anywhere. We publish articles, books, and guides to help you learn how to meet the needs of seniors. The providers and services listed under “Senior Services” are here to help with any retirement or eldercare need.” – Thomas Day, Director

https://www.longtermcarelink.net/

https://www.carecompare.com/senior-care-advisors/louisiana/baton-rouge/

https://www.elderlawanswers.com/how-likely-are-you-to-need-long-term-care–15501